The capital markets posted mixed results in the second quarter of 2023.

The broad fixed income market (BB US Agg) returned -0.8% in the quarter as rates increased across the maturity spectrum. The index is down 0.9% for the year.

The U.S. large cap market (S&P 500) continued its rally and finished the quarter up 8.7%, with the one-year return now up 19.6%. Growth stocks outperformed value stocks in the quarter (returning 12.8% versus 4.1%) and are now ahead by 15.6% over the last year. U.S. small- and mid-cap stocks continued to underperform, returning 3.4% and 4.9%, respectively.

International developed underperformed their U.S. counterparts over the trailing three months and are in line over the trailing year. Emerging market stocks were barely positive for the quarter and year and significantly underperformed all other asset classes. Mainland Chinese stocks returned -10.7% in the quarter, while Latin American stocks returned 14.0%. The U.S. dollar (U.S. Dollar Index) was flat against most other currencies in the quarter and is now down 2.2% over the previous twelve months.

Given the surprisingly strong equity gains in the quarter, all the diversified portfolios posted positive returns.

Our Select portfolios outperformed their Global counterparts while performing in line with their secular benchmarks for the trailing three-month period. For the trailing 12-month period, our Select strategies have outperformed their respective benchmarks, while our Global strategies have underperformed.

All our asset class strategies, with the exception of U.S. Large Cap, outperformed their benchmarks in the quarter.

Over the trailing twelve months, all our asset class equity sleeves significantly outperformed their secular benchmarks.

The emerging markets sleeve outperformed the MSCI Emerging Markets Index over the trailing three (12.1% versus 0.9%) and twelve (29.2% versus 1.8%) months. The main contributors to the outperformance were the portfolio’s lack of exposure to Chinese stocks (which were down over 10% in the quarter and comprise nearly 30% of the index) and overweight to Latin American stocks (which were up double digits). These same factors helped the portfolio outperform over the trailing one year. We exclude state-owned enterprises (like those in China) where significant human rights abuses are known to occur. Security selection also benefited performance. In particular, the portfolio’s Brazilian, Chilean, Mexican, and Indonesian holdings performed very well relative to the index.

The stock market has been surprisingly strong so far in 2023. It seems that investors have shrugged off most of the concerns they had about inflation in 2022 and are optimistic that the U.S. may avoid a recession. We feel that investors have been overly confident, and we would not be surprised to see a correction in the coming months, especially in overvalued areas of the market like the mega-cap, tech stocks. Those stocks have been responsible for 80%+ of the recent market gains and are very overvalued based on P/E valuations. The rest of the market is reasonably valued.

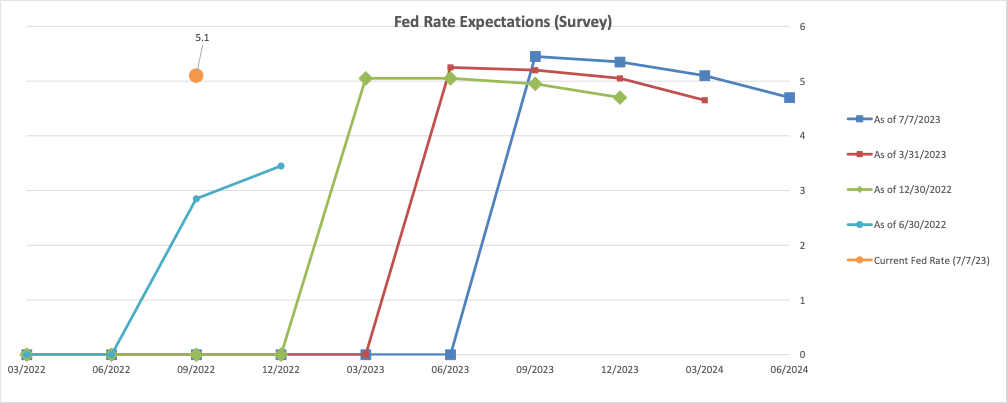

Inflation, Money Supply, and Central Bank Response – The May CPI month-over-month reading was 0.1%, in line with expectations. Year-over-year inflation has fallen from over 8.0% in the previous quarter to 4.0% and will likely fall more as outsized readings in May and June 2022 drop off. However, inflation will likely pick up again towards the end of the summer, or at least will remain well above the Federal Reserve’s 2.0% target. Based on this and Chair Powell’s recent comments, we should expect more rate increases this year, with a terminal rate now above 5.5%. We will continue to closely monitor monthly inflation readings and the Fed’s response as this will undoubtedly impact capital market returns and volatility in the months and years ahead.

GDP, Yield Curve, Employment, & Consumer Confidence – The final first quarter GDP figure was raised to 2.0% from 1.3%. Although this was stronger than expected, we are in a trend of slowing growth which could get worse especially if personal consumption, business investment, and home building continue to slow/decline going into 2023. In addition, the yield curve remains heavily inverted (which generally occurs leading up to a recession) and the Conference Board’s leading index has never declined this much in six months without a recession. With inflation still running hot and the labor market remaining strong, the Fed will likely keep rates high to try to bring down inflation. Therefore, the odds of a recession occurring over the next few quarters have greatly increased. We will continue to keep a close eye on growth figures going forward.

Corporate Profits – As we make our way through 2023, there are signs that earnings are starting to fall. Indeed, 1Q2023 profits fell the most since 4Q2020. We expect profits to continue to fall, particularly given the impact of higher interest rates and potentially slowing consumer demand. We will continue to keep a close eye on corporate earnings as this will impact equity performance going into 2023.

Darrell Jayroe, CFA, CFP, CKA, serves as Inspire’s Senior Portfolio Manager responsible for leading the firm’s Investment Committee, as well as serving as Lead Portfolio Manager for Inspire’s ETFs and SMA strategies. Darrell has been with the firm since 2016.

Prior to joining Inspire, Darrell was a Vice President and Sr. Portfolio Manager for the Bank of Oklahoma trust department for 12 years where he was responsible for managing accounts for high net worth families, trusts, foundations and institutions. Darrell started his career as an investment advisor in 1994 with PaineWebber in Oklahoma City.

Darrell received a B.A. and Masters degree from Southern Nazarene University in Bethany, Oklahoma. He is a CFA (Chartered Financial Analyst) charter holder and is a CFP® (Certified Financial Planner®) licensee. He is a member of the CFA Institute and a member and Past President of the CFA Society of Oklahoma. He is also a member of Kingdom Advisors and holds the CKA® (Certified Kingdom Advisor®) designation.

Darrell and his wife, Beth, have been married since 1982 and have two daughters, a son in law and two grandchildren.

Tim Schwarzenberger, CFA, is a Portfolio Manager with Inspire Investing and has served in the industry since 2000. He previously served as Managing Director at Christian Brothers Investment Services (CBIS), where he was an integral member of the Investment Team responsible for implementing the firm’s strategy development, portfolio construction, and Catholic investing initiatives.

Information on this website does not involve the rendering of personalized investment advice but is limited to the dissemination of general information on products and services. A professional adviser should be consulted before implementing any of the options presented. The information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed.

The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. Registration as an investment advisor does not constitute an endorsement of the firm by securities regulators nor does it indicate that the advisor has attained a particular level of skill or ability.

Different types of investment involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client's investment portfolio. No client or prospective client should assume that any information presented and/or made available on this Website serves as the receipt of, or a substitute for, personalized individual advice from the adviser or any other investment professional.

National Admin Office: 3597 E Monarch Sky Ln, Suite 330 Meridian, ID 83646; Phone: (877) 859-6383 Investment advisory services offered through Inspire Advisors, LLC, a Registered Investment Advisor registered with the SEC.

© Copyright - Inspire Advisors, LLC