The markets were whipsawed again in August, with most asset classes and sectors experiencing losses. The broad fixed income market (BB US Agg) returned -2.8% in the month as rates increased across the maturity spectrum. YTD the Agg is down 10.8%. The equity markets were up the first half of the month and then retreated due to investor concerns about inflation and central bank response. The US large cap market (S&P 500) returned -4.1% in August, bringing the YTD performance to -16.1%. US small and mid-cap stocks performed in line with US large-caps for the month and are ahead ≈1-2% YTD. International developed equities performed in line with their US counterparts, while emerging markets equities significantly outperformed and were one of the few sectors with positive returns (+0.4%). Latin American stocks lead the way as oil and other commodities prices remained elevated in the month. The US dollar (US Dollar Index) was also a standout for the month, returning 2.2%.

With the selloff in August, all of the Core Satellite portfolios posted negative returns. On a relative basis, the strategies outperformed their benchmarks, with the Select strategies outperforming their Global counterparts.

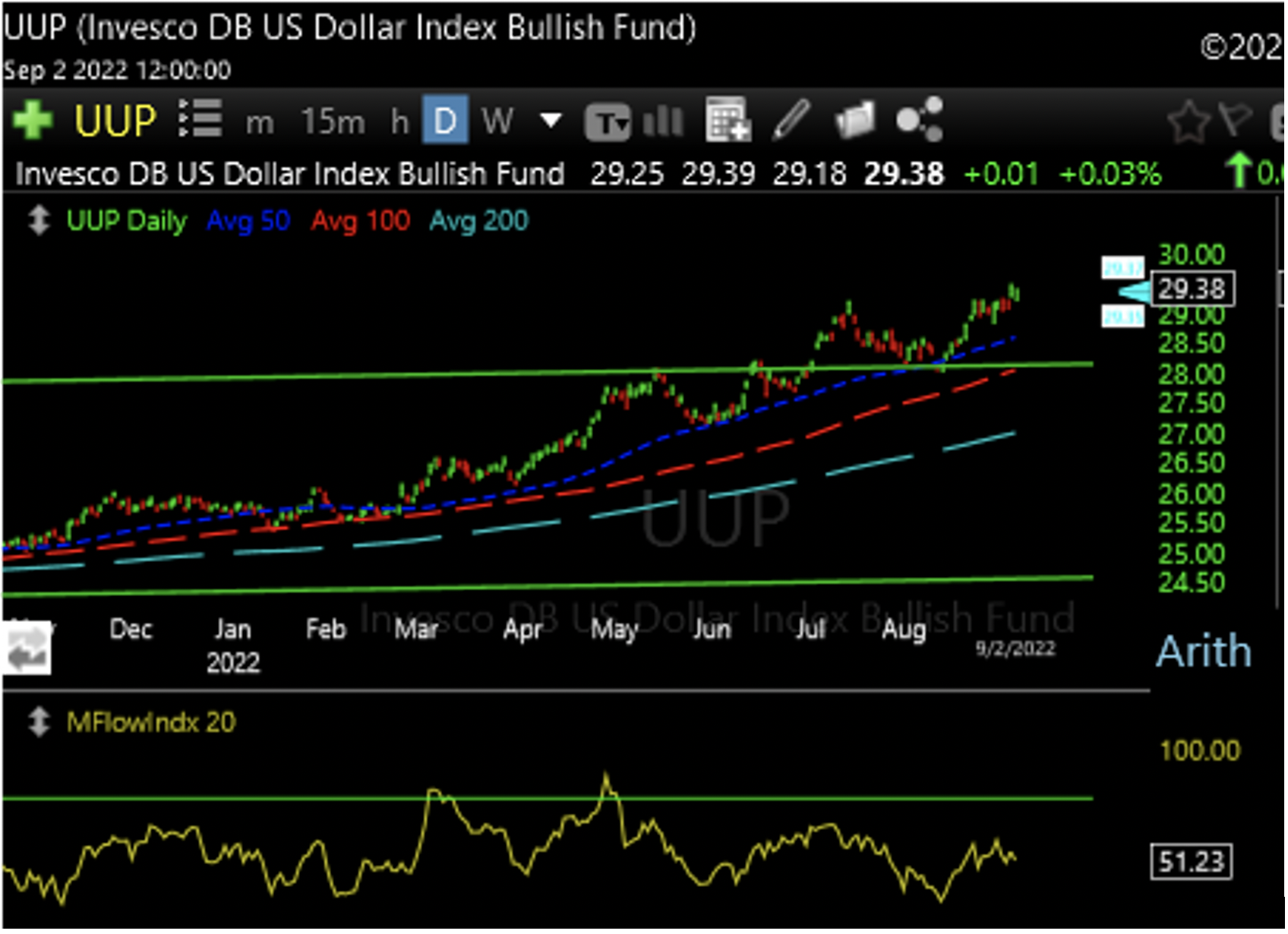

The “Core” portion of the portfolio underperformed for the month due to weaker performance from our international equity and US large cap positions (WWJD, BLES, and BIBL) relative to the MSCI World Index. This was partially offset by strong relative performance from our US SMID position (ISMD). The “Satellite” portion of the portfolio outperformed as the allocation to UUP (Invesco DB US Dollar Index Bullish Fund, which tracks the performance of the US dollar relative to a basket of six major currencies) outperformed the broader market (UUP was up 2.9%, while the broader market was down -4.2%). On the fixed income side, the 70/30 strategies have been negatively impacted by rising rates. However, on a relative basis, the portfolio outperformed the BB US Agg for the month given its shorter duration to the benchmark (4 versus 6.8 years). On a YTD basis, IBD has outperformed the BB US Agg by over 2.0%.

Our move to add exposure to the US Dollar in recent months has proven to be beneficial as equities and bonds have both been under pressure. There are no equity sectors that have technical indications for positive returns, so for now we will continue using UUP as exposure to the US Dollar for our satellite position.

Our technical analysis is indicating that stocks are likely in for another steep decline, possibly equal to the entire decline we have experienced thus far in the year. There is significant technical weakness in the price charts for equities and bonds, so we advise investors to prepare themselves mentally to weather another sharp drop in asset prices – and also prepare themselves to take advantage of low prices as a buying opportunity when risk abates, trends flip positive, and the market rebounds from an oversold position. We will continue to monitor the market structure closely for such an opportunity, and until then we will keep as much of our powder dry with allocations to asset classes and sectors which we believe should fare better during the next expected leg down in the market.

Quadrant Interpretation:

· Strengthening: Performance < benchmark but momentum is UP

· Leading: Performance > benchmark, relative strength is UP

· Weakening: Performance > benchmark, relative strength is DOWN

· Laggard: Performance < benchmark and momentum is DOWN

· Benchmark: S&P 500 (S&P 500 Sectors)

Tactical Risk Management posted a small loss for the previous month, but even though returns were slightly negative, they were less negative than the broader market thanks to the defensive positioning we have held since last year.

August was an up and down month for stocks, with a nearly perfect symmetry between the continuation rally in the first half of the month and the ensuing selloff during the second half of the month. The bond market, on the other hand, was under constant pressure throughout the entire month as inflationary pressures continue to wreak havoc for fixed income.

Tactical Risk Management has been invested in a defensive posture with high credit quality corporate bonds with short to intermediate durations, as well as opportunistic hedge exposure that seeks to earn return from the few market segments that offer compelling buy signals over the short term. There is nothing in the charts to indicate that the selloff is near an end, and until we see risk abated TRM will continue to remain on defense.

The rally in stocks during July and the first half of August was a partial retracement of the larger decline markets have experienced most of the year. As the chart shows, there is a well defined downtrend channel that has contained prices for the entire time, and the recent rally turned on a dime right at the upper boundary line, confirming again the validity of the down trend. We will continue to watch price reactions to the upper and lower trend lines of this channel as one of many signals we will need to confirm that the selloff is reaching an end, which is not something we are seeing yet.

Our previous TRM strategy update mentioned that the July-August rally in stocks was likely a second wave corrective move against the previous wave one down. That analysis seems to have been proven correct so far as the price chart formed a classic “ABC” pattern three wave correction, terminating at the upper channel line and promptly resuming downward action with vigor. Since that second wave peak, prices have declined in rapid succession, suggesting that wave three down has begun.

Third waves are the longest and strongest waves in Elliot Wave analysis, which portends a very rough September and October for the market as we expect prices to accelerate with crushing downward momentum. There will be some sharp, but brief, rallies along the way, but until the full five wave pattern is complete, Elliot Wave analysis tells us that the overall trend will be decidedly bearish. It is our view that the technical indicators are pointing to a decline of at least another 15% from current levels (targeting S&P 500 3400 or lower) before the next meaningful uptrend begins. As such, we will continue holding defensive positions in TRM and advise investors to prepare themselves mentally for riding out another precipitous decline in stocks – and then to be prepared to take advantage of low prices as a buying opportunity prior to what we expect will be a sharp uptrend as markets slingshot back from oversold territory.

At Inspire Advisors – The Chandler Team, we focus on three main strategies that are diversified and actively managed “in house” by The Chandler Team. Below is an overview of how the strategies performed, what changes were made during the month, and what our expectations are for the month ahead.

How did the CW Active strategies perform for the month?

· CW Active Protection: -1.96%

· CW Active Balanced: -2.01%

· CW Active Growth: -2.06%

How did the static blended benchmarks perform for the month?

· DJ U.S. Conservative: -3.30%

· DJ U.S. Moderate: -3.19%

· DJ U.S. Aggressive: -3.25%

How did the individual holdings (assets classes) perform for the month?

· US Large Cap Stocks (BIBL): -4.93%

· International Stocks (WWJD): -7.48%

· US Small/Mid Cap Stocks (ISMD): -4.73%

· US REIT Index (USRT): -5.12%

· US LT Treasuries (VGLT): -8.11%

· US IT Treasuries (VGIT): -3.53%

· US ST Treasuries (VGSH): -0.86%

· US ST Treasuries FLT (USFR): +0.20%

· Gold (GLD): -4.34%

· Div. Commodities (GSG): -2.34%

· Mortgage Back Sec. (RISR): +3.62%

What changes were made to the investment strategies during this month?

No changes were made to the investment strategies during the month of August. During the first half of August, our indicators moved into what looked like the beginning of an uptrend, but we decided to stay more defensive, which paid off as the “down trend” for stocks, real estate, and longer-term treasuries resumed the second half of the month. The out-performance of the models compared to the blended benchmarks is due to our more conservative positioning regarding stocks and real estate.

What are our expectations for the month ahead?

We will keep our eye on the current trend direction and see if any asset classes change direction enough to warrant an increase in our allocations. Due to higher-than-expected inflation, interest rate increases (which we believe will be higher than the FED is predicting), and possible recessionary pressures due to rising rates; we do not anticipate high returns for the more growth focused assets classes the remaining part of 2022.

We are researching other items to possibly add the models that would do well in rising interest rate situations as well as increasing inflation scenarios. If we find something that our team believes offers a good risk/reward opportunity, we will add it to the models in proportion to their expected risk offset potentials.

We will also be keeping an eye on the duration of our bond holdings and making sure that they are in line with our future inflation and interest rates expectations.

For the month of August, FEVR fell by -3.13% vs -4.08% S&P 500 and -1.99% USA Momentum (MTUM) benchmarks. GLRY dropped -1.72% vs -3.17% S&P 400 Midcap and -1.99% USA Momentum (MTUM) benchmarks. FEVR had strong returns in Energy, notably Devon Energy (DVN), and food-related companies. Notable decliners were within the tech sector, as continued pressure from higher rates persist. Within GLRY, Qualys Inc, a cybersecurity firm, saw double digit growth, while consumer discretionary company, Yeti, had comparable downside with weakened consumer spending expectations.

As the market continues moving toward a reduced-risk posture, we remain committed to executing our FEVRR process and find investors attractively performing, biblically responsible investing options. As markets also seek risk in high-performing sectors, like energy, we continue to be risk managers and ensure our investments are not only screened for biblical values but also strong balance sheets and flexibility in these challenging times

For the month, the Inspire Tactical Balanced ESG ETF (RISN) returned -2.11%. The fund outperformed the S&P Target Risk Moderate Index (AOM) by +1.84%, which returned -3.95% (according to Morningstar.com). We attribute this performance to the very conservative allocation that the fund held for the month with regards to the percentage of stock compared to treasuries and gold.

The management team diversified the “defensive” allocation of the fund into floating rate, short and intermediate term treasuries due to an increase in momentum in those asset classes. The fund is also holding a small allocation to gold and large cap US stocks. The overall stock market (S&P 500-SPY) increased by -3.50% for the month.

For the last twelve months, the Inspire Tactical Balanced ETF (RISN) returned -10.65% and has outperformed its benchmark (S&P Target Risk Moderate Index) which returned -11.55% (according to Morningstar.com). We attribute this outperformance to continued defensive position held by the fund so far in 2022.

We continue to monitor the US Large Cap stock market to see if the trend/momentum remains in a downward direction. The US Large Cap stock market staged what could have been the start to a new “up-trend”, however due to other economic factors including raising interest rates, inflation and recession fears, the markets turned back into a “down-trend” the second half of August. This bear market bounce was similar to what we saw in March which is what made our investment committee remain in a more defensive position than we otherwise would have given how much the markets ran up in July.

We continue to monitor the price movements of gold. We currently hold approx. 5% in gold. Gold has been in a downtrend according to our charting system and if this trend continues, we may reduce the fund’s gold allocation even further or even remove it completely while we wait for an up-trend in Gold to resume.

We continue to monitor the US Treasury holdings within the fund. We diversified the funds allocation to treasuries at the end of July and will continue to monitor that allocation and make changes as we see the trends unfold. We anticipate holdings reduced duration or floating rate treasuries for the foreseeable future as the trend of raising of interest rates seems to be something that will remain through the end of 2022.

Issachar lost -0.29% in July (a flat month), while the IQ Hedge Multi-Strategy Index lost -1.14%, so Issachar outperformed its benchmark. Issachar held positions in the solar, oil, gas, chemicals, and biotech areas, but the market was not rewarding us for taking risk, so we sold them. Issachar currently holds an ETF that shorts junk bonds and another that is long natural gas. We do not have much conviction anywhere else since the market appears to be headed lower after the Fed's aggressive measures to reduce inflation.

Powell is fighting inflation by raising rates and decreasing its balance sheet. I see no reason to hold bonds that will go down in value while the Fed promises to raise rates until inflation is "under control." Higher rates also make it more expensive and less profitable for companies to borrow money for expansion, especially when the economy is mired in a recession. A stagflationary environment of higher rates and slower growth is not conducive to increased earnings or P/E expansions. Therefore, I have decided to focus on the short side, expecting to make money if stocks decline. Shorting emerging markets has caught my attention, and I plan to act accordingly if things unfold as I expect.

The Fed is finally doing what it promised: to unwind its balance sheet fighting inflation. When the Fed reduces its balance sheet, they remove liquidity from the system, and the whole system thrives on liquidity. The Fed has reduced its balance sheet by $139 billion since 4/19/22, and the S&P 500 is down 11%. I do not see an easy way out of stagflation other than a prolonged recession/depression. The market has always bounced back to new highs, but this time may be different. Please support and pray for God-honoring men/women to get us out of this problem irresponsible leadership has caused.

Liquidity is declining, and the market has responded negatively. I believe the market is headed lower to test the June 16th bottom. This high inflation and negative GDP growth (stagflation) environment will likely create life-changing losses for investors who do not manage/respect risk. I have been managing risk for over 32 years, and this is the worst D.C. leadership of incompetence I have ever seen. We need a change of God-honoring leaders to right the ship before it sinks. I expect to profit in this environment by making money on the short side (betting prices will fall). I pray for God's Wisdom to be on our leaders. Thanks for Your Trust, and Praise Jesus!

For the foolishness of God is wiser than men, and the weakness of God is stronger than men.

1 Corinthians 1:25

Financial professional use only. Do not distribute to the public.

IMPORTANT RISK INFORMATION

Mutual Funds involve risks, including the possible loss of principal. An investment in the Fund may not be appropriate for all investors. The Adviser's judgment about the attractiveness, value, and potential appreciation of particular asset classes and securities in which the Fund invests may prove incorrect and may not produce the desired results. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses.

Investors should carefully consider the investment objectives, risks, charges, and expenses of the Issachar Fund (LIONX). This and other important information about the Fund are contained in the prospectus, which can be obtained by calling 1-866-787-8355. The prospectus should be read carefully before investing. The Fund is distributed by Northern Lights Distributors, LLC, member FINRA/ SIPC. Horizon Capital Management Inc. and Inspire Investing are not affiliated with Northern Lights Distributors, LLC. NLD Review Code: 4027-NLD-09/06/2022

Information on this website does not involve the rendering of personalized investment advice but is limited to the dissemination of general information on products and services. A professional adviser should be consulted before implementing any of the options presented. The information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed.

The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. Registration as an investment advisor does not constitute an endorsement of the firm by securities regulators nor does it indicate that the advisor has attained a particular level of skill or ability.

Different types of investment involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client's investment portfolio. No client or prospective client should assume that any information presented and/or made available on this Website serves as the receipt of, or a substitute for, personalized individual advice from the adviser or any other investment professional.

National Admin Office: 3597 E Monarch Sky Ln, Suite 330 Meridian, ID 83646; Phone: (877) 859-6383 Investment advisory services offered through Inspire Advisors, LLC, a Registered Investment Advisor registered with the SEC.

© Copyright - Inspire Advisors, LLC